Hire More Staff

- Hire new employees to support your business growth

- Make sure payroll is covered so your workers are paid on time

A working capital loan is a business loan that intends to cover normal operating expenses. When businesses have lower revenues compared to their expenses, they often take a working capital loan so that their expenses will be covered.

Working capital also offers support for short-term business activities that are happening on a smaller scale. In most cases, these loans cover occupational expense shortfalls that occur occasionally and ensure the continuity of business operations.

In general terms, a working capital loan will be a smaller amount and have a shorter repayment period compared to other business loans. The repayment is usually made within a year.

Slow paying receivables and seasonal shortfalls cause cash or revenue shortfalls and the primary objective of working capital loans is to cover the shortfalls. Having enough working capital is crucial in deciding the success or failure of your business. Hence it important to understand why you need working capital, its uses, and ways to ensure that you have enough working capital for your business to run smoothly.

When used properly, working capital loans can be greatly helpful in overcoming occasional cash flow shortages or making the best use of business opportunities before they are gone.

![]()

![]()

![]()

6 Months in

Business

Fico Score Over

575

Equipment Quote

From a Vendor

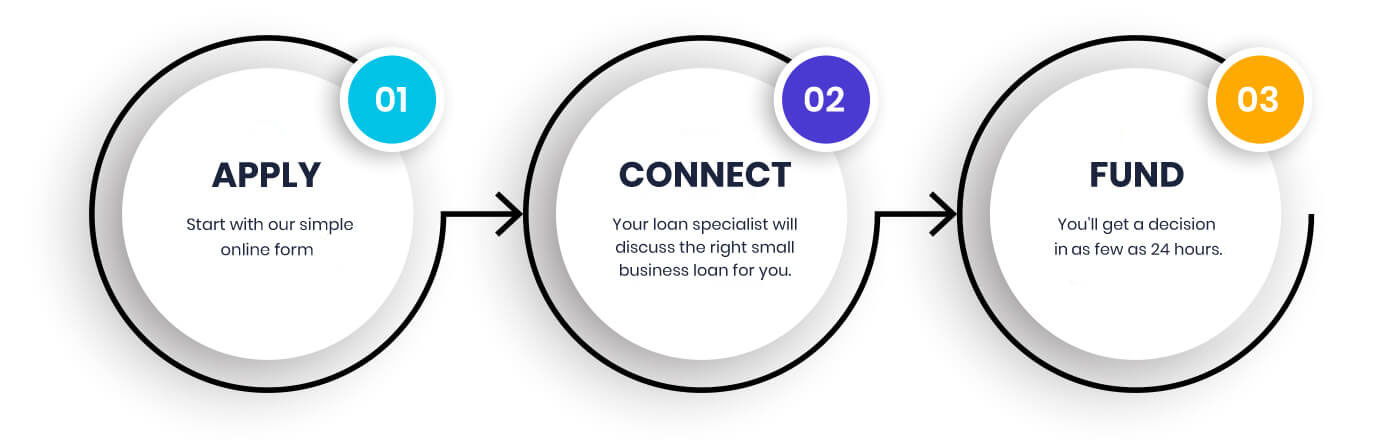

Securing the funds your business needs in order to continue running smoothly is easy with financing options from Building Block Capital. Our application process is easy, fast, and secure. In only a couple of minutes, you can apply for a customized loan for your small business.

After you finish applying, one of our loan specialists will contact you so we can learn a little more about you and your business. Your loan specialist will help answer any questions you have about the loan process and help you determine which loan is the right fit for you and your business. Our high approval rates and quick decisions make it easy for you to get back to running your business.

or call

Building Block Capital offers a personalized approach and will help guide you and answer any questions you may have with our expert loan specialists. Our funding process is made easy in order to get you the money you need quickly to help cover your business expenses.

Fill out our quick online application with a decision in as little as 24 hours

Experienced Loan Specialists help you choose the right financing option that is fit for your business.

No collateral requirements, with easy, automatic payments

“Working capital loan” is a generic term that relates to any type of loan used by businesses to get smaller capital in a timely manner by agreeing to pay back in a shorter time period to make specific purchases like real estate or machinery.

Take a look at the most popular working capital loan types:

The loan is usually provided by a bank or credit union. Short term loans differ from lines of credit in terms of the interest rates and disbursement method. They often have fixed interest rates and the loan is made in a lump-sum disbursement, indicating that all amount is paid one time. The loan has a predefined repayment period that is usually one year or less.

Short term loans are usually secured loans, meaning that you will have to pledge collateral that can cover the loan amount in cases of default. However, some banks may give you unsecured loans but that is determined by your history with the lender and the amount you have requested as a loan. Getting a loan approval is a subjective process and the loan terms are often negotiable.

It is a type of financial transaction in which a business decides to sell some or all of its accounts receivables to a third party at a discount rate. With invoice factoring, a company gets immediate cash for its unpaid invoices by discounting the full invoice amounts. In this transaction, the company is in fact giving up a portion of the revenue it earned and it is a downside associated with this.

Invoice factoring is expensive and requires research to get maximum quotes from lenders practically. Rates will vary from lender to lender.

It is important to realize that invoice factoring and invoice financing are two different things. The term “invoice financing” describes a kind of asset-backed lending in which the collateral that you pledge to obtain a short-term loan is your unpaid invoices.

A merchant cash advance/MCA is a type of credit that is usually used by businesses that provide goods and services by accepting credit card payments. The processor of the business’s credit card or other financing company will be able to offer advance amounts to the business based on a portion of the past monthly dollar volume of the merchant’s credit card sales. The advance amount that is received by the business is then paid back to the funding company as a portion of the future credit card sales of the business.

Suppose the average monthly credit sales of a merchant is $50,000, the financier may give $20,000 as advance and automatically take 40% of all credit card sales in the next month until the merchant pays the advance fees. This is an extremely simplified example. Repayment schedules and funded amounts are based on formulas provided by the credit card processor.

Third parties may also be involved in merchant cash advances. In that case, the business grants the third party lender the authority to get the payments directly through fixed payment plans or from credit card sales.

A business line of credit is a cross between a business credit card and a business loan. Similar to a loan, an unsecured business line of credit is a source of business financing used to cover general business expenses. There isn’t a lump-sum disbursement method involved in a line of credit; the business owner borrows only what they need and is required to pay interest for the borrowed amounts only.

Ready cash that can be used immediately is the feature of a line of credit. With that, a business owner can learn the interest rates in advance and have a fixed amount in cash to draw upon. In addition to that, you are only obligated to pay interest on the amount that you have borrowed and used.

If using a line of credit, your chance of getting larger amounts and lower interest rates are increased if you make sure to pay it back in a timely manner. By proactively establishing a business line of credit, you can improve the financial stability and use the line of credit to meet your working capital needs in the future.

Applying for a business line of credit when your business is in a good condition and company finances are stable, your application has a higher chance of being accepted.

A bank overdraft facility that is known better in the name “bank overdraft protection” allows you to draw amounts more than what you have deposited in your bank account. In this arrangement with the bank, you aren’t required to pay any overdraft penalty fees and only have to pay interest for the overdraft amount. This is especially useful when there are unexpected shortfalls in your account because your accounts receivable pay slower. Being offered an overdraft facility helps you pay your bills on time, avoid penalties, and stay on good terms with your bank.

Small Business Administration Loans

The US Business Administration is a well-known source of working capital loans. Many business owners have no idea about SBA loans providing smaller loans for businesses. The SBA 7(a) loan is particularly suitable for smaller amounts used to procure working capital. The 7(a) working capital program has a range between $5000 and $5 million.

It is important to note that the SBA does not follow the practice of lending money directly to businesses and instead they work with approved lenders for guaranteeing loans to businesses. Strong credit is important to be qualified for an SBA loan and you will also have to fill out some paperwork as well. The repayment terms of SBA loans are more in favor of the borrowers and the loan also has lower interest rates.

The primary reason why many businesses take working capital loans is to ensure their trouble-free operation. However, there are some important things that you should know about working capital loans and common situations when businesses are in need of this type of loan.

It is important to make a mental note of the cost of borrowing when you are taking a business loan. Now business loans have become specialized to suit different circumstances and users. Short-term borrowing often has more associated expenses, which is why it is important to understand the cost and plan how you are going to repay the loan. The following are some typical circumstances when companies decide to take working capital loans:

Consider a boat rental company in the Northeast US. The period between late spring and early fall will be its busiest season but from late fall to early spring, it will even be forced to stop its operations. However, it should still maintain its facilities, pay rent, and pay the staff. There are hardly any chances for a business of this kind to earn revenue during the off-season and it becomes necessary to borrow in the early spring for buying new equipment, doing repairs, and hiring staff for the upcoming busy season.

It is almost impossible to predict exactly where a business will be in the near or far future due to its unpredictable nature. Infrastructure or inventory may at times become damaged due to some disasters, machine breakdowns, or some equipment getting lost or stolen. Even if the inventory is insured, the insurance claims won’t be paid immediately in most cases. Having access to ready cash during emergencies can do a lot to ensure the survival of your business.

Growth opportunities that come to many small businesses have to be taken advantage of without wasting time. Whether it is a chance that you get to move to a new location or renovate the physical space of your company, it is important to make a quick decision and for that, you need cash-on-hand.

Many small businesses sometimes experience an unexpected upsurge in growth. Suppose a restaurant sees the reservations tripling with a good review written by an influential food blogger. Would they be able to handle the growth spurt by managing to have enough staff, food, and space? Or perhaps an influential blogger writes about a hotel mentioning it as an amazing destination. Would they be able to handle the overnight success? The success of your business is something that is not that easy to get, and cash flow should never be in the way of your business’s success.

You might have heard many savvy retail business owners telling that they earn money by buying the merchandise and not by selling it. It is more of an idiomatic expression and does not focus on the literal meaning of the phrase. The phrase stresses the role of purchases made at the right price in increasing profit margins. This could mean getting bulk price discounts, buying more popular items, or getting a chance to buy rare merchandise. With working capital loans, you can make the best use of the supply opportunities of this kind.

This is not to be mistaken for seasonal fluctuations. It is quite a serious issue in the service industry. Many service businesses follow the practice of sending invoices for services. If there is a default, it is often impossible for the service providers to reclaim their service unlike sellers of physical goods. Generally, service invoices take longer to collect and if your receivables are lagging behind your payables by a big margin, you might have to consider getting a working capital loan.

Equipment financing is a small business loan that is mainly used for buying business equipment like vehicles, machinery, computer, or any other business equipment. Business owners will be able to use the newly bought equipment and machinery as collateral for the loan, thereby preserving on-hand cash.

If you are looking for a working capital loan, you would be thinking about the amount that is ideal for your needs. The loan amount is ideal if it is enough to pay your regular bills and debts if you have any. Business owners should have a clear idea of how to make use of their business assets to aid their progress rather than just using them for paying bills and debt.

You can develop a clear understanding of your financing needs with the help of a ratio for a working capital loan. Using a simple formula, business owners will get a clear idea about what their exact requirements are in terms of working capital. It is called the working capital ratio. The rule is not hard to understand and consider the following even if your company is different. The working capital formula is:

Suppose your company has $62,500 as assets and the current liabilities amount to $50,000. 62,500/50,000=1.25. Thus your working capital ratio is 1.25.

The working capital is assessed by creditors, lenders, and partners to get an idea of how healthy the business is. If the net working capital is negative or less than 1.0, it means that the business has significant liquidity issues or lacks enough productivity when compared to the current debt. Despite any reason, the issue is considered as a serious warning sign.

Businesses can make use of the working capital equation to find the sweet spot between paying existing debts and bills, all the while preparing for future business growth.

The equation helps you figure the amount that you have to borrow in a working capital loan.

Making an overall assessment of your liabilities as well as your short term assets can help you develop a better understanding of your working capital needs. The working capital checklist is a quick guide that helps you determine your cash position and decide whether you need a working capital loan.

Cash position

Liquid Investments

Prepaid Expenses

Accounts Receivable

Inventory

Accounts payable

Short-term debt

A working capital loan is similar to any other business loan and has to be dealt with in similar ways. Before you formulate the plan to apply for the loan, ensure that you can justify the purpose of the funds. After you arrive at the conclusion that there is a justification for the loan, the next step is to define how you are going to use the money. Never spend money in ways that will not make any contribution to the outcomes you intend.

While taking any loan, find out if the loan will improve your business in some way. If you cannot find out anything, better avoid taking the loan. In addition to that, you should be confident in your business’s ability to repay the loan.

Before applying for a working capital loan, you should understand the true cost associated with it. Also, you need to find out if there are better ways to finance the working capital needs of the business. In most cases, a working capital business loan will help in the growth of your business and overcome cash flow issues but you have to exercise caution in selecting the finance company.

Speak to a Loan Specialist