Questions? Call Us Anytime

(877) 386-3035

Questions? Call Us Anytime

(877) 386-3035

Business Loans with Bad Credit

Getting Business Loans with Bad Credit

It can be quite a challenging task to bag a business loan as a business owner who doesn’t have great credit. Businesses that are bothered by this situation have many options if they know the right things to look for and the right steps to take.

How to Get a Business Loan While Having a Bad Credit?

You may have to pledge collateral if you wish to get a business loan with bad credit. Lenders will provide loans to some borrowers if the borrowers can pledge liquid assets or future accounts receivable. This is for securing the repayment of the loan. Business owners with bad credit will have to pay higher fees and interest than those with good credit.

What Does A Bad Credit Business Loan Mean?

A bad credit business loan is the financing offered to a company or an individual that has a bad credit score. Most lenders depend on the rating system called FICO score. If your FICO score is less than 500, you are said to have a bad credit score. Loans that are given to companies or individuals with a bad credit score are called sub-prime loans. As the risk of default is more in this case the interest rates of the loans granted to entities with bad credit are usually high.

Business Loan with Bad Credit

Getting a business loan with bad credit is quite a challenging task, but not impossible. With many new sources of funding like crowdfunding and alternate lenders in the marketplace, securing finances for your business has become much easier than before.

Most lenders take the following factors into account while granting business loans: the credit score of the owner, the business credit score, annual revenue, and negative events like bankruptcies.

It is important to keep in mind that having a bad credit score means you will have to pay higher interest rates, get smaller loan amounts, and will have to repay the loan within a shorter term unlike when you have a good credit score. Before you apply for a business loan, you can check your business credit profile and see if there are any ways to improve your credit score. You won’t be able to change everything but knowing what position you are at will help you figure out the appropriate sources of a bad credit business loan.

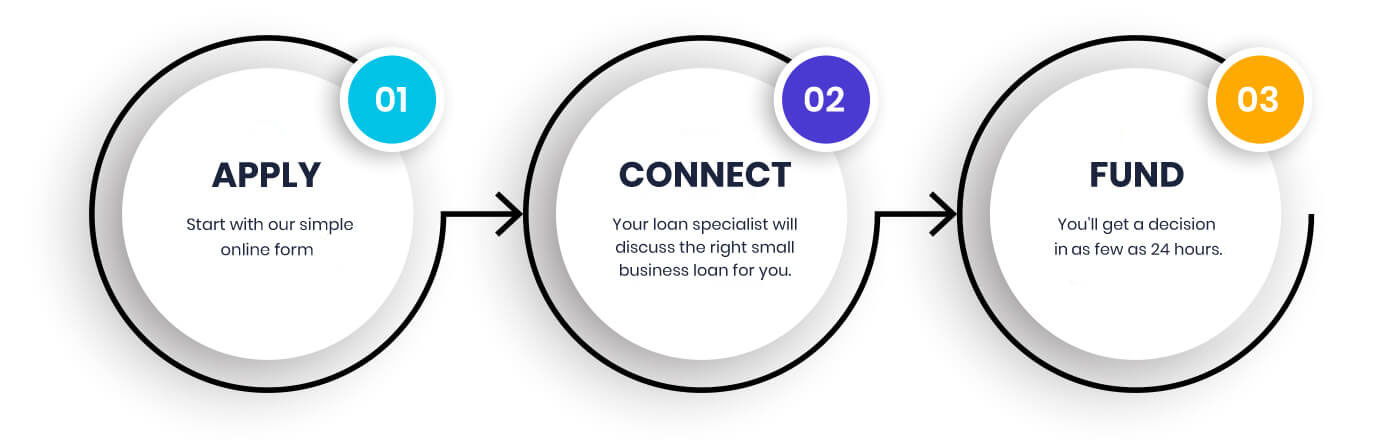

How to Apply

Securing the funds your business needs in order to continue running smoothly is easy with financing options from Building Block Capital. Our application process is easy, fast, and secure. In only a couple of minutes, you can apply for a customized loan for your small business.

After you finish applying, one of our loan specialists will contact you so we can learn a little more about you and your business. Your loan specialist will help answer any questions you have about the loan process and help you determine which loan is the right fit for you and your business. Our high approval rates and quick decisions make it easy for you to get back to running your business.

or call

Why Building Block Capital

No matter what industry you're in, we understand that you sometimes need funding to continue running your business.

With a custom-tailored approach to your unique business needs, we deliver the financing you need in order to continue growing.

Experience With Multiple Industries

We’ve supported thousands of businesses for their financing needs

Trusted by Businesses Like Yours

Over $150 million in funding to more than 40,000 businesses nationwide

Personalized Experience

Financing solutions and payment options tailored to your specific needs

Quick & Easy Application Process

Fill out our quick online application with a decision in as little as 24 hours

Loan Specialists Who Care

Experienced Loan Specialists help you make the right decision

Stress-Free Lending

No collateral requirements, with easy, automatic payments

What Are The Best Sources Of Business Financing With Bad Credit?

Below shared are some of the best sources of financing if you have a bad credit score.

Business Credit Cards

When compared with conventional bank financing, business credit cards are far easier to be approved. They usually have lower credit score minimums but have lower borrowing amounts and higher credit scores.

Invoice Factoring

Invoice factoring is a finance method that companies with unpaid invoices find useful. In this method, you sell your accounts receivable at a discount for a cash amount.

Merchant Cash Advances

In Merchant cash advances, businesses will sell their future credit card sales or other business receipts to the party that is providing funds to the business in exchange for a cash advance. Merchant Cash Advances are not like normal loans and they lack a fixed repayment term. The repayment in this case is made through smaller regular payments.

Credit Score And Probability Of Being Granted Business Loans

Getting a business loan with bad credit is always a challenging task. To get a business loan when having a bad credit score, understanding the causes of your bad credit score is an essential first step. The sessions yet to come in this article, will cover the basics of business credit and some of the ways for improving your credit score.

Most of the lenders will check the business owner’s FICO credit score and personal credit history to decide whether or not to provide financing and loans to a small business. With small businesses, lenders often adopt this approach because the business is a typical extension of the owner’s financial well-being.

Bad business credit can have an adverse impact on the credit terms that your business will be offered by your suppliers. It may also prevent your company from getting new important business because your customers will lack confidence in your financial stability.

Credit Rating Agencies and FICO Scores

Three major credit rating agencies, Equifax, Experian, and Transunion uses a standardized FICO score for calculating your credit score. However, these companies often report different FICO scores for individuals and that could be due to the multiple factors associated with their access to your credit activities, the reporting cycle they adopt, and timelines for collecting data on your credit activities.

What is Considered a Bad Credit Score?

The credit score usually falls in the range between 300 and 850. Credit scores below 500 are considered bad credit risks. The credit scores allow the leaders to establish a grading system on the ways in which individuals manage their credit.

Even though many factors are taken into account while calculating your credit score, two factors account for about 65% of your credit score. These are:

- Payment history

35% of your credit score is influenced by your payment history. Missing payment due dates on your loans or credit cards will cause a significant decrease in your credit score. Making payments late can affect your credit score adversely, particularly when the payment is more than 90 days late.

Making your payments on time is very important

Credit tip: If you know you won’t be able to make the payment on time, get in touch with your creditor and request them to give some more time to make the payment. Creditors may help you by extending the payment cycle and not reporting the delayed payments to the credit agencies.

It is important to keep in mind that the information that your creditors give is being used by credit reporting agencies. Therefore, it is very important to have a close relationship with your credit card companies, bank, and other finance lenders.

- Existing Credit Amount

30 % of your credit score is determined by your existing credit. It is usually evaluated as the ratio of your existing debt payments to your monthly gross income. Consider for example your monthly income is $10,000 and you have $5000 in debt in monthly payments of $500. Then your debt to income ratio is 5%. It means that 5% of your monthly income is being used for paying your debts.

Debt to income ratio formula

DTI=Total monthly debt payment amount/gross monthly income

To assess your available income for paying present and future debts, your DTI is selected as the general guideline. When you take on more debt, your DTI ratio keeps increasing whereas your available capital for paying the debt will decrease. At one point your monthly debts will become greater than the funds available for making payments. Lenders will use this ratio to determine your ability to take on additional debt in a safe way.

Credit Rating Agencies And Business Credit Ratings

Like the personal credit rating evaluated based on your FICO score, there exists a business credit rating system. According to Nav, a business credit support website, 45 percent of small business owners have no idea that a thing called a business credit score exists and 85 percent of them lack the knowledge to interpret their score.

Equifax and Experian are the most popular credit rating agencies. The largest of business credit rating agencies however is Dun& Bradstreet.

Different from consumer credit ratings that make use of a standardized FICO score, business credit ratings are usually based on a non-standard scoring system which is different for different credit rating agencies. To view business credit reports, you have to pay a fee even if you are the owner. This is very different from the case of consumer credit reports.

Finally, the information provided by the business owner partially influences the business credit reports. In the coming paragraphs in this article, we will address the steps that can be taken to improve your credit score and remove errors.

Top-Rated Business Credit Agencies And Scores

Equifax

The business credit scores at Equifax fall between 101 and 992, with lower scores indicative of higher credit risk. A bankruptcy filing is represented by a score of 0.

Experian

The business credit scores fall between 1 and 100. Lower scores are indicative of higher risk.

Dun& Bradstreet

The analysis of D&B is much complicated although it is more public. They evaluate creditworthiness by making use of six sets of scoring classes. The D&B Delinquency Predictor Score evaluates the possibility of a business paying its bills on time in the next 2 years. The scores fall between 101 and 670 and a higher score indicates that there is an increased possibility for the business to pay its bills on time.

How can you Improve Bad Business Credit?

Similar to consumer credit history, business credit reports include information that is collected from various sources. It is not very rare to find outdated or inaccurate data in a business credit report. Hence monitoring your credit profile at the aforementioned rating agencies is important.

Steps To Improve Your Credit Scores

- Get copies of your business credit report and note any information that is inaccurate or more than 3-5 years old. Credit rating agencies usually have policies regarding the length of time for which credit data will remain active on your account. When the time limit expires, they may remove the outdated information. The policies of all agencies aren’t the same.

- If you happen to find any negative credit actions, contact the credit agency. Have adequate proof of your findings and submit requests to get that information corrected or removed.

- Ask your vendors, customers, and suppliers to report the payments and delivery of goods and services that you made on time. All companies do not automatically give reports to credit rating agencies.

- Talk to the suppliers who have submitted negligent payments on your account. Find out if they will agree to some alternative payment arrangements and if they accept your request, try to keep the word. After many months of making on-time payments, ask the suppliers to report that to the credit agencies. Trying to make positive changes to negative accounts indicates your seriousness in improving your creditworthiness.

- Attempt to reduce the amounts you owe people and the use of credit. One of the best ways to improve your credit profile is by paying off debts. It is quite normal to have business debts but excess outstanding debt for a long period of time may indicate financial stress.

- Separate your business from your personal finances. To do this, you can create a legal corporate entity like an LLC or a corporation.

- Get an Employee Identification Number from IRS so that your business gets legal tax status. You may be provided EIN for free on the IRS website.

- Start a business bank account to show a record of your deposits and balances to prospective lenders.

- Make your payments on time. Even if your payment history wasn’t that good, try to change that and make paying on time a top priority.

- Do not just make the assumption that your business will have a credit profile with major credit reporting agencies. In some of the cases, you will have to initiate the process.

Getting A Business Loan With Bad Credit

Bad business credit will increase your borrowing costs and affect your insurance premium adversely. Moreover, you will find it difficult to find new clients. However, your company will not be disqualified from getting a loan just because of bad credit.

There are various sources that can offer bad credit business loans. They include invoice factoring, alternative lenders, crowdfunding, and merchant cash advances. You need to take adequate steps to keep track of your credit score and improve it. Your business suffering from bad credit does not mean that there is no way you can change it or that you are expected to accept it. You can take some immediate steps for improving your business credit so that you will be able to enjoy the benefits that a strong credit rating has to offer within a short time period.

Speak to a Loan Specialist