Hire the Best Staff

- Use a working capital loan to recruit and attract quality staff

- Hire the best staff to help you manage your insurance agency’s customer service and finances

Independent insurance brokers have several challenges. The broker will have to get new clientele, maintain their annual and mandatory continuing education requirements, get new makers, handle associations with carriers, and deal with their cluster or network affiliation.

One of the strongest and ever-growing industries is the insurance sector. The professional count in the segment is also growing. An insurance agency’s past stability and growth performance can signify that it is very likely to repay an insurer. This means it is a potentially good move for the company to grant you a loan. Individuals may not consider insurance the most attractive field to work in, but the levels of employment here are growing without much change.

![]()

![]()

6 Months in

Business

Fico Score Over

575

Equipment Quote

From a Vendor

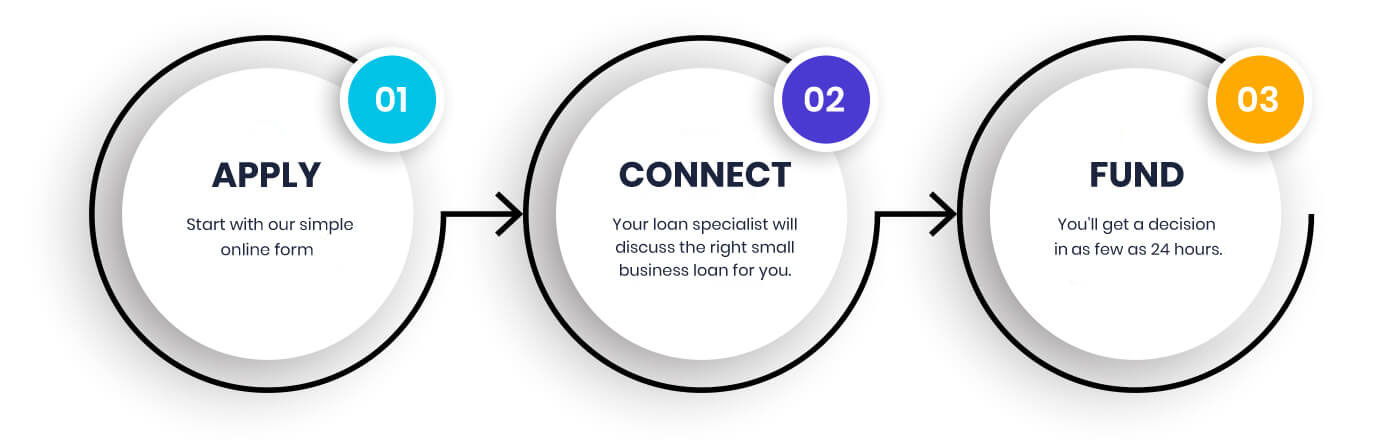

Securing the funds your business needs in order to continue running smoothly is easy with financing options from Building Block Capital. Our application process is easy, fast, and secure. In only a couple of minutes, you can apply for a customized loan for your small business.

After you finish applying, one of our loan specialists will contact you so we can learn a little more about you and your business. Your loan specialist will help answer any questions you have about the loan process and help you determine which loan is the right fit for you and your business. Our high approval rates and quick decisions make it easy for you to get back to running your business.

or call

When looking into the needs of your insurance agency, you want to work with a lender who has experience in working with other insurance agencies before. At Building Block Capital, we understand that receiving funding for an insurance agency can be difficult. As a business owner, you occasionally have to wait for clients to pay for your services. Insurance agency business loans from Building Block Capital do not require drawn-out paperwork. Speak with one of our friendly, expert loan specialists to get more details about our business loans.

We have experience working with insurance agency business owners

Over $150 million in funding to more than 40,000 businesses nationwide

Financing solutions and payment options tailored to your specific needs

Fill out our quick online application with a decision in as little as 24 hours

Experienced Loan Specialists help you make the right decision

No collateral requirements, with easy, automatic payments

Policyholders own these companies. The policyholders pay month-wise premiums, which the management holds and invests, plus they share the losses and profits. Every single policyholder has a say in the administration and operations of the insurer. Anyhow, most of them are not only uninformed about their status and legal rights under the corporate structure, but they also do not take part in the company voting process.

The insurance carrier is set up to meet a specific group’s mutual insurance requirements for a particular cause. Benjamin Franklin established America’s first-ever mutual insurance carrier, named ‘the Philadelphia Contributionship’, in 1752. This company is in operation even now.

MassMutual and Liberty Mutual are two more examples of insurance providers. These companies offer a broader variety of investment and insurance products, plus they advertise broadly. This advertising option is a potentially great advantage to insurance brokers who sells to their clients. As the broker, you have to think about the financial strength of an insurance carrier when deciding to represent that company’s goods and services.

Stockholders own this form of an insurance company. Each of the biggest stockholders in the insurance companies is a bigger institution, not an individual investor. No policyholder shares the losses or profits of the company. Prudential and MetLife are two examples of insurers.

America’s insurance sector net premiums amounted to $1.20 trillion three years ago. Life and health insurance companies accounted for 52% of the amount as the premiums, whereas property and casualty insurers accounted for the rest of it, as per S&P Global Market Intelligence.

Property and casualty insurance mainly comprises automobile, commercial, and residential insurance. Net insurance premiums recorded for the P/C insurance segment amounted in number to $558.20 million back then.

Private health insurers and government insurance carriers are part of the health insurance segment. It is considered a separate segment. Life and health insurers and property and casualty insurance carriers write some amounts of health insurance too.

The US and its territories were home to 5,977 insurers in 2016, which included 247 RRGs, plus 2,538 P/C, 872 life annuity, 858 health, 85 fraternal, 55 title and other insurance companies, as per the NAIC.

Around $510 billion of the US’s 2016 GDP came from insurance providers and insurance-related activities, as per the Bureau of Economic Analysis’s data.

The American insurance sector gave work to 2.6 million individuals in 2016, as per the Department of Labor’s information. Of the 2.6 million individuals, 1.5 worked for insurers, which included L/H insurance carriers, P/C insurance companies, and reinsurers. The rest worked for insurers, insurance brokers, and insurance-concerned enterprises different from those two.

P/C insurers’ invested assets and cash totalled $1.59 trillion four years ago, as per S&P Global Market Intelligence. Life and health insurers’ invested assets and cash amounted to around $4 trillion back then. The overall invested assets and cash for both segments were around $5.5 trillion. Most of the aforementioned assets were issued as bonds.

Life and health insurers and property and casualty insurance providers paid about $21 billion as insurance premium taxes back then, as per the Department of Commerce’s data.

P/C insurance providers paid out around $22 billion as property losses, associated with calamities occurred in 2016, as per Verisk Analytics’ Property Claims Services unit. The year 2016 saw 42 catastrophes, 3 more than in 2015.

Given how deeply insurance affects nearly every aspect of a person’s life and a business, it is obvious why the product is considered very recession-proof. Lending money to an agency that deals with insurance products is a pretty good risk as far as a financial institution is concerned.

The next segment has extensive industry information, published to aid you in understanding the insurance market size and identifying the market segmentation.

Economic fluctuations adversely affect the industry. With this in mind, let us discuss a few macro-economy-related trends that can impact the usual insurance business cycle.

For instance, when gas prices go up, people may decide against either purchasing another automobile or the residence expansion they have been intending to do. This results in insurers selling fewer policies than what they would otherwise trade.

Rates of interest can also impact insurance premiums. Insurers rely on TVM, a concept that the money that you presently have will be worth much more in the future. This means insurers are encouraged to delay paying insurance claims, for the whole time that it is reasonably possible. This is because insurers get considerable profits through appreciation or interest on the total premiums they receive from those who hold the policy. In the event of interest rates being low, insurers could not earn that much, and they might have to raise premiums to remain profitable.

The premiums that your clientele pays you, and how efficiently insurers pay their claims, can result in you keeping that customer or them seeking a different broker.

The insurance segment and the economy go hand in hand as both need each other, in some way, for stability and prosperity.

The field of insurance brokerage is very competitive. You might find that it is possible to invest much money, effort and time in acquiring new clientele, only to witness the client approaching a different broker. Client retention matters as much as client acquisition to an American insurance agency.

Keep in mind that there exist nearly unanimous industry reports on the practices that are deemed the most effective for customer retention. As per the Insurance Journal:

The rates of retention are 95% on average concerning individuals who have a vehicle and residential policies from the same provider, and 92% regarding those who combine rental and vehicular policies. On the other hand, these average just 83% regarding mono-line automobile customers, and just 85% with regards to policyholders who never combine their homeowners and auto insurance.

The takeaway from the above is that you being an agent should give multiple coverage options that are not just competitive, but that also present value to clients. Spending on education, promotion, and other forms of informative media can make the earning potential of your insurance agency bigger.

Take the effort to go through and research the industry best practices, plus be familiar with your market more closely. Thus, you will get a better idea about your capital and funding requirements for your agency.

An insurance agency is likely to require some extra capital at the start. Recruiting people, continuing education, licensing, getting an office, plus providing utilities, furnishings, and infrastructure will all cost much.

SBA Loans

These are usually regarded as one of the most preferred loan options for small businesses. An SBA loan offers optimal rates of interest and repayment terms for an insurance agency that seeks a term loan. The Small Business Administration works with qualified financial institutions, and it partially guarantees loans to protect the interest of the institutions. It can guarantee as much as 85% of the loan amount, letting the institution provide the borrower with higher amounts on optimal terms.

Be warned: it is not easy to be eligible for an SBA loan, plus it may require submitting much paperwork. Anyhow, given the low financial risk related to the insurance sector, you can expect a high rate of approval from SBA’s loan scheme.

You would like to focus closely on SBA’s 7(a) scheme. There are characteristics in this loan program that go with the requirements of insurance professionals. Some of these characteristics are the greatest possible loan amounts, repayment terms and rates of interest, plus flexibility regarding the utilization of the money.

Things To Anticipate:

Conventional Bank Loans

These traditional lenders are the primary source of financing for small businesses even today. Almost every business might find that it is possible to have some amount of funding from the bank through which they already do business transactions.

Bigger local and national banks generally have loan schemes specialized for professionals from the insurance field. The high rate of success for insurance agency activities makes insurance broker loans an appealing proposition for American banks. Therefore, these banks will provide insurance agencies with favorable rates of financing.

Bank terms may not be favorable to the same extent as those of SBA loans, but you may anticipate having the following from the product.

Loan amount: Between $30,000 and $5 million

Rates of interest: Starting from 7%

Repaying term: As many as 10 years

Time for loan approval: 4 weeks or so

Business Credit Line

The term ‘LOC’ refers to the money borrowable up to an extent that is predetermined. It acts as a blend of a credit card and a loan for business purposes. Similar to a usual business loan, a non-collateralized credit line offers the financing that you can utilize for usual business expenses. Similar to the credit card, it does not have any lump-sum distribution; you may borrow the amount you require and may pay interest on only it. Banks and other lenders offer business lines of credit.

Is your credit profile strong? If yes, you could negotiate not only loan repayment terms but also interest rates. The rates are likely to vary much from one lender to another, so you should shop around.

Things To Anticipate

Loan amount: Between $10,000 and $1 million

Rates of interest: Between 7 and 25%

Repayment term: 6 to 60 months

Time for loan approval: Just a single business day

Non-Bank Loans

Financial institutions like Building Block Capital offer business loans to insurance professionals, with speedy approval. There are shorter loan approval cycles, less paperwork, and lower borrower credit standards at these institutions as compared to the aforementioned funders.

Anyhow, insurance professionals may expect to see high rates of interest and charges related to the lower standards and faster approvals. If you need a quick financing solution for your agency, a non-bank lender might just be appropriate for you. Alternative lenders must follow regulations different from banks, so it is important to peruse the loan documents before you agree to their terms.

Things To Anticipate

Loan amount range: $2,500 and $250,000

Loan repayment term: Between 3 and 18 months

Rates of interest: Starting from 10%

Loan approval time: Only a single business day

Understand your market for an idea about what your borrowable amount is and the amount you have to borrow. If it is not clear, it might be more advisable to choose a product such as a business LOC.

Speak to a Loan Specialist