Bigger Loan Sizes

- Most traditional lenders balk at loans over $100,000

- Commercial funding allows qualified applicants to secure up to $500,000 for business needs

Usually, the phrase ‘commercial loans’ refers to many different forms of debt instruments utilized for business causes. Financial institutions including banks issue commercial loans as debt instruments, which necessitate borrowers to repay principal amounts, interests, and applicable charges over a stipulated period.

Standard Medium-Term Loans

These are some of the most prevalent forms of loans available for small-sized entities. These can be forms of general-purpose debt instruments repayable in 1 to 5 years. The amounts can fall between $25,000 and $5 million.

Long-Term Commercial Loans

These are generally bigger amounts utilized for significant capital expenditures or property purchase, repaid over 5 to 10 years. Principal amounts are usually more than$1 million.

Short-Term Loans

These are generally payday advance-type debt instruments, meant to pay for short-term costs or to offer more capital when seasonal revenue subsides. Loan amounts fall between $5,000 and $250,000.

SBA Loans

The US-based Small Business Administration has a low-interest, long-term loan program, which the organization partly guarantees. The lenders that participate in the program, most commonly conventional banks, issue SBA loans. The products mostly come as conventional term loans because the lenders issue these as one-time distributions to borrowers.

Equipment Loans

These forms of financing for businesses are meant especially for the purchase of fresh equipment, by utilizing this asset as collateral.

In practice, several big American banks usually relate commercial loans to the buying, refinance, or upgrading of commercial properties. Commercial loans may be a generic phrase, but business owners must know that there exist several options for business financing. Business loans may be made differently, but there exist more sources for acquiring commercial loans. Loans are made differently to cater to the varied requirements of an entity. In the following segment, we will look at the best-known commercial loan options, how the function of the loan, and in what way to obtain these.

![]()

![]()

6 Months in

Business

Fico Score Over

575

Equipment Quote

From a Vendor

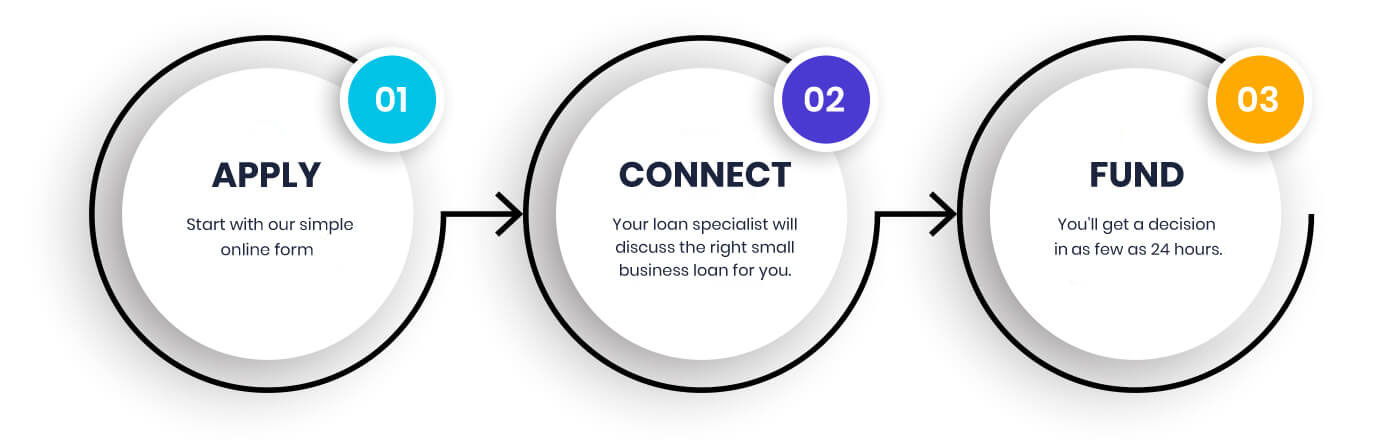

Securing the funds your business needs in order to continue running smoothly is easy with financing options from Building Block Capital. Our application process is easy, fast, and secure. In only a couple of minutes, you can apply for a customized loan for your small business.

After you finish applying, one of our loan specialists will contact you so we can learn a little more about you and your business. Your loan specialist will help answer any questions you have about the loan process and help you determine which loan is the right fit for you and your business. Our high approval rates and quick decisions make it easy for you to get back to running your business.

or call

No matter what industry you're in, we understand that you need equipment for your business, help pay for inventory, payroll and more.

Our business loans don’t require drawn-out paperwork. Speak with one of our expert loan specialists today to learn more about we can help you.

We’ve supported thousands of businesses just like yours to finance equipment needs

Over $150 million in funding to more than 40,000 businesses nationwide

Financing solutions and payment options tailored to your specific needs

Fill out our quick online application with a decision in as little as 24 hours

Experienced Loan Specialists help you make the right decision

No collateral requirements, with easy, automatic payments

Generally, the loans are utilized to finance either operational expenses related to business acquisition/ expansions or big capital acquisitions. The phrases ‘commercial loans’ and ‘commercial financing’ can allude to commercial property debt instruments. Anyhow, it is possible to use commercial financing in an array of ways, plus more and more forms of it are categorized as loans for general purposes.

The acronym ‘OpEx’ refers to operational expenses, which are related to the continuing costs that a business bears to run its core activities. One of the examples of OpEx is perhaps the costs to fulfill higher payroll requirements, cover exceptional seasonal costs, or buy products utilized in manufacturing.

The term ‘CapEx’ refers to funds that companies utilize to purchase, improve and maintain tangible assets. Usual CapEx can include fresh equipment purchase, upgrading enterprise technology, inventory and amenities, and real estate. Even so, commercial loan programs come with longer durations, bigger principal amounts, and big capital expenditures. The durations are like the ones related to property purchases, whereas the expenditures include capital items or machines with a longer estimated lifespan.

Medium to big financial institutions usually gives commercial loans. The borrower’s profile is often a business owner having a solid credit record (a credit score of 680 or higher), a minimum of $250,000 as yearly revenues, and entities that have been operating for many years. Besides, these forms of loans mostly require pledging some level of collateral against the debt instrument in case a default occurs.

For instance, Bank of America’s minimums to have a commercial property loan are 24 months in operation under the same ownership and $250,000 as annual revenue.

There exists a high level of requirements to be eligible for commercial financing, and it comes with bigger loan amounts. Therefore, financial institutions will offer more advantageous borrowing terms to the businesses that qualify for it. Shared below is a list of the usual commercial financing terms.

According to the demanded loan principal, banks may be the primary source of loans for businesses. Local banks give almost every commercial loan to businesses. Virtually every business owner approaches local banks for this form of financing. Having a settled business banking association with a financial institution in your area might boost your possibility of obtaining a loan, should you have a long history of steady business activity. Are the local bank and its loan officer familiar with your company and you? If yes, they would be more ready to consider your loan demand considerably.

Anyhow, for bigger loan amounts of $5 million or more, it is perhaps not the right idea to seek commercial financing from a local bank. Before you apply for it, contact your bank manager to know what loan sizes he or she will serve.

SBA offers loan programs assured with a guarantee through banks, and these are some of the most appealing options for commercial financing. The loans are suitable for capital acquisitions, so these are highly popular options among those who seek commercial financing.

SBA’s 504 loans maybe your best option if you are seeking a commercial property loan of $350,000 or more. SBA’s Express and 7A loan programs usually have longer repayment terms and relatively smaller down payments.

SBA loans generally provide not just lower rates of interest but also lower costs for borrowing. Anyhow, the loans can have trickier eligibility requirements and more documentation as compared to other financing programs. These are called ‘last resort’ loans. In most loan programs, SBA necessitates an entrepreneur to have used up every other financing option to be able to apply for its guaranteed loan.

The business loan market is very specialized. It is not unusual for bigger banks to keep an individual or a whole department devoted to a certain form of a loan. For instance, there are separate loan divisions or teams devoted to particular forms of commercial property lending activities, categorized according to industry type, at Building Block Capital. Complex financial terminology can easily confuse you, so you must understand the jargon about the loan appropriate for your requirements and qualifications.

A loan officer may ask you what you want a loan for. It is usually the first rational question that you must be asked. The professional will ask it to discover the form of a loan that best fits your requirements. If they do not do it, raise it at an early phase of the discussion and ask which form of loans are provided for your purpose. It will be useful to know those products as you compare loan programs of different financial institutions.

You should look at the commercial financing options available to you before making the right choice for your business requirements. Then, you may want to diligently plan your loan application strategy. Just be ready and take the time to assess the needs and your business position.

After looking at the options, consider choosing the loan program that is most likely to be approved. As talked about earlier, there is a different set of qualification requirements for every single commercial loan scheme. Anyhow, a few fundamental eligibility criteria are common among loan providers.

The indicator that matters the most for the provider is a company’s annual revenue. It will let the lender know whether a business borrower can pay back the specific loan amount that they apply for.

Generally, loan providers will establish the lending amounts as a small portion of that business’s average revenue. According to other criteria involved in decision making, it could be between 12% and 18% of the said revenue. With advanced models that are based on millions of business loans and considerable experience, lenders have conceived loan formulae to account for unexpected revenue fluctuations and costs.

This means one who owns a business having $1 million as annual revenue, may anticipate receiving a loan of between $120,000 and $180,000. While the above is only a ballpark figure, it reflects real averages.

Loan providers will look to check the borrowing company’s revenues in many ways. These lenders will tell that business owner to submit their P&L statement, plus personal and business tax statements. Most of the time, lenders require borrowers’ tax returns because these records offer them the best possible idea of their revenue activity.

Your bank account statements will let a lender know how cash flows into and out of your company. Lenders wish to verify whether you are handling your business finances correctly. For instance, repeat overdrafts in the banking account of your business may signify bad fiscal handling of cash flow-related issues.

Do not forget to maintain a single year of steady, if not growing bank balances at the least. Lenders wish to ensure that you possess enough capital to go through fluctuations in your business cycle and that you being the owner is ready for these unexpected events. This shows judicious business management.

Lenders also assume that business borrowers must have filed 2 years of their tax returns, which demonstrate enough profits to repay principal amounts and interest and have some amounts of surplus even then. It is called ‘Debt Service Coverage Ratio’, and banks usually require business borrowers to have between 1.1 and 1.5 as DSCR over 2-3 years.

Several lenders would only like to know whether you have a viable business idea. More than 80% of every business doesn’t succeed in the first 24 months in operation. Unsurprisingly, almost every lender will necessitate a business to have been in operation for at least 24 months to be eligible for their commercial loan product.

This period would be particularly important if you apply for a long-term form of financing. Has your business been in operation for just 24 months, and are you applying for the product with a 30-year repayment period? If yes, approving your loan would be a big risk for that lender. This is because that 2-year-old business is not likely to last 3 decades. If it has been in operation for over 24 months, it would be a lesser credit risk for the lender concerned.

A person and their business’s credit rating may have a big effect on loan determination. The credit score is a sign of one’s trustworthiness because it shows their credit management history.

Simply put, financing providers regard one’s credit history as a good sign of how they will manage their finances in the future. The providers will look for potential red flags like delinquencies, tax liens, bankruptcies, write-offs, and similar derogatory things.

With one’s credit score, every lender can get a profile about their credit use and an idea about whether they apply for credit somewhere else. Credit checks are likely to lower an individual’s credit score, albeit they have not yet borrowed money from another source.

So, it is not a good idea to apply for credit to discover your eligibility when you are yet to perform some preparation. Acting as per some of our guidelines mentioned here might aid you in improving your odds of finding the appropriate loan and having the loan application approved.

Speak to a Loan Specialist