Hire More Workers

- Address hiring needs for larger projects with construction business financing

- Replace workers as needed to solve for the high turnover rate in the construction industry

Business owners usually wonder whether to acquire or lease the area where they run their business. It is among the trickiest things to decide for one who owns a business. The commercial land or building that you own can be an extremely costly asset gradually during a long period. When managed correctly, it can help to guarantee your business’s longevity.

Knowing the fundamental information of commercial property loans is likely to considerably affect not just your business’s bottom line but also its future security.

A person who owns a business should contemplate purchasing the commercial land or building, in which they run their business, instead of leasing it, for two main reasons. Firstly, doing so will confirm that they can keep operating their business for the entire time they hold that property. The other main cause of buying it is to keep having the monetary benefit for a long period.

Shared below is a list of factors to consider when choosing between the options of leasing and purchasing the property. You may utilize some of the following information to have an idea about this choice’s comparable costs. You should deal with certain hurdles when trying to obtain a commercial loan, like credit qualifications and down payment. Even so, it will be an excellent measure to understand the expenses related to every single scenario.

![]()

![]()

Buying the property will result in its value accrual to your entity gradually over a long period. Well-established businesses, and those who are sure of their business’s long-term position, should consider paying monthly installments to a commercial property loan. This is because doing so will let them build real estate value, and it will possibly yield them more value by means of property appreciation.

Purchasing commercial properties can also let business owners use the assets in a more flexible way. For instance, they will then have the option of subdividing the space as business situations change, paving the way for extra revenue.

6 Months in

Business

Fico Score Over

575

Equipment Quote

From a Vendor

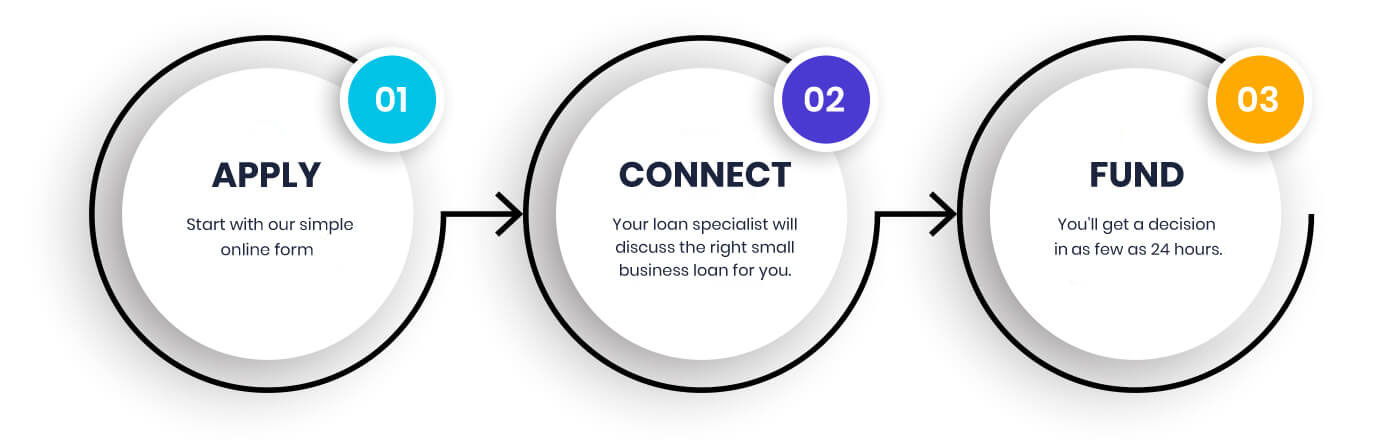

Securing the funds your business needs in order to continue running smoothly is easy with financing options from Building Block Capital. Our application process is easy, fast, and secure. In only a couple of minutes, you can apply for a customized loan for your small business.

After you finish applying, one of our loan specialists will contact you so we can learn a little more about you and your business. Your loan specialist will help answer any questions you have about the loan process and help you determine which loan is the right fit for you and your business. Our high approval rates and quick decisions make it easy for you to get back to running your business.

or call

There's something unique when it comes to commercial real estate businesses, and that is that majority of your customers come through referrals, and payments are made after the sale is made. Due to the nature of the business, many commercial real estate businesses find that getting a small business loan from traditional lenders is rather difficult. At Building Block Capital, we have the experience to understand how commercial real estate business works and are able to offer you higher approval rates than a traditional lender.

We have experience with commercial realtors and developers

Over $150 million in funding to more than 40,000 businesses nationwide

Financing solutions and payment options tailored to your specific needs

Fill out our quick online application with a decision in as little as 24 hours

Experienced Loan Specialists help you make the right decision

No collateral requirements, with easy, automatic payments

You should buy commercial property mainly to confirm that it is possible to keep operating your business at the same place for however long you’d like. It is particularly true for almost every retail operation. Restaurants are among the best examples of it.

How often have you discovered the tale of an entity that had been flourishing for many years in a single location only to abruptly shut down? This occurs more frequently than you might think because of an increase in their property lease rate.

Commercial property landlords will seek to make as great returns on their real estate as possible. So, a commercial land or building’s owner will generally renew their tenant’s lease at market price, when they should do it. Rentals of commercial properties can go up exponentially.

The owner may have to change their business place if they cannot keep investing in the existing property after their lease term, in the best-case scenario. The worst-case scenario is them having to shut down their business as the fresh lease terms are beyond their capability to get a profit from the investment.

Business owners must be extremely cautious when arriving at lease agreements, focusing much on their business operations’ future. A business owner may sign their first-ever lease agreement usually when they lack clarity regarding its future and perhaps wish to avoid signing the long-term contract. It is unfortunate that the aforementioned situation usually happens.

Leasing has the risk of the building or land’s owner not extending your lease terms and selling the property on which you run your business instead. You being a commercial property tenant may relinquish much control over your future business location.

The phrase ‘commercial property’ refers to a tangible asset utilized for business causes. The local zoning rules that designate properties for many different kinds of commercial applications, define the phrase more. Examples of commercial-type assets include office spaces, retail stores, restaurants, salons, gas stations, warehouses, and production facilities.

Commercial property loans are meant specifically for not just buying fresh real estate for business causes but also making additions or upgrades to this property. Legally established companies, such as LLCs or S corporations, are the ones that mostly apply for these loans.

To get this loan, the property concerned itself is utilized in the form of collateral against possible repayment failure, with its provider putting a lien against that property. The term ‘lien’ refers to the legal entitlement of the loan provider to seize that property if the borrower fails to repay the loan.

Lenders will usually necessitate one who borrows their commercial loan to pay 20% to 30% of the purchase rate as its down payment. Remember that this down payment is possibly negotiable, according to the provider and your credit profile. Shared below are pie charts that show standard loan-to-value (LTV) ratios.

SBA 7(a) Loans

These are the products of a US bank or another financial institute, which participates in the Small Business Administration’s 7(a) loan scheme. The SBA partly guarantees these loans, and the scheme aids businesses in buying or refinancing the owner-occupied- and commercial-type properties. It is interesting that most of these products are utilized for business working capital.

CDC/ 504 Loans for Commercial Properties

The SBA loan scheme offers approved small entities fixed-rate and long-term financing, to purchase long-term assets for either modernization or expansion. The loan assists existing and new businesses in acquiring or refinancing the owner-occupied real estate. Similar to the aforementioned 7(a) products, the SBA backs these loans. A certified development company makes the loans available to businesses.

Conventional Lender-Based Property Loans

A bank, insurer, or some other financial organization issues a conventional commercial property loan/ mortgage, which is not federally backed. Conventional commercial property loans are utilized to buy or refinance shopping centers, retail centers, industrial warehouses, and other real estates.

Bridge Loans

Also termed swing loans, commercial bridge loans are a kind of financing that can let you bridge the gap between present and future fiscal situations. These are usually utilized up to the time it is possible to arrange more permanent business financing, like a mortgage.

Swing loan terms are generally some months to a year, but these can occasionally be beyond 12 months. You should use the commercial land/building that you either possess or will soon buy, as collateral for a commercial swing loan. So, it is a collateralized form of the loan. Lenders tend to approve the loan on the basis of how much the collateral concerned is worth.

Speak to a Loan Specialist